Contents

- Central Bank Digital Currencies (CBDC)

- At What Stage Are the Digital Turkish Lira Studies?

- The Rise of Buy Now Pay Later (BNPL)

- Shopping Credit Usage Becomes More Common

- AI-Driven Personalized Financial Services

- Number of Users is Increasing in Mobile Payments

- Open Banking & API Integration Becomes Widespread

- We Will See Embedded Finance Applications More Frequently

- Decentralized Finance (DeFi) and the Use of Blockchain

- Basic Working Principle of DeFi

- The Rise of Neobanks

- Developments in Regtech Will Become Even More Important

- How is Regtech Used in Banking and Fintech?

- The Rise of Banking Technologies as a Service

- Payment Orchestration Platforms Will Become Game Makers in 2024!

- Payment Orchestration Market Volume Expands

- Businesses Aware of the Benefits of Payment Orchestration Platforms

- Payment Orchestration Platforms Open the Door to Payment Options for Businesses!

- Payment Orchestration Platforms Reduce Cart Abandonment Rates for Businesses

- Businesses Reduce Costs with Payment Orchestration

- Fintech Leaders – Expert Opinions

New generation financial services are undergoing a rapid digital transformation with constantly evolving technologies. While there is great innovation and adaptation in the fintech field, fintech technologies continue to redesign financial habits that have been around for years.

Artificial intelligence, machine learning and blockchain applications, which are among the popular topics of recent times, affect the future of fintech while also strengthening its efficiency and security.

Fintech trends such as digital currencies, shopping loans, buy now, pay later models, mobile payment solutions, smart contracts, neobanking and orchestration solutions are creating convenient and secure alternatives for both businesses and customers.

In light of all these exciting developments, we have brought together the fintech trends that will shape the future of financial technologies and that companies of different sizes should put on their radar in order to achieve more sustainable growth.

Also, don’t forget to review the “Expert Opinions” we compiled from leaders and experts in the fintech field in the last section of the study!

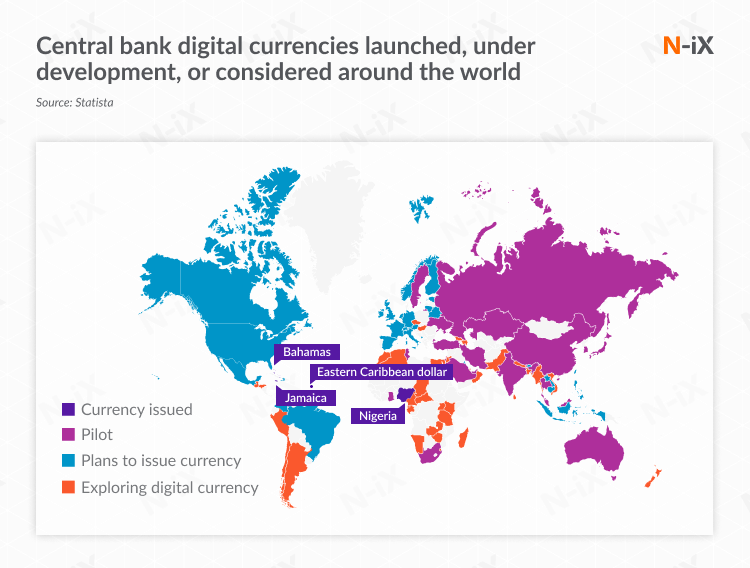

Central Bank Digital Currencies (CBDC)

Central Bank Digital Currencies (CBDC), which are accepted as legal tender and can be defined as digital assets, offer a controlled structure, unlike decentralized and untraceable cryptocurrencies. In this case, central bank digital currencies are gaining popularity around the world.

Many countries have implemented centralized digital currencies, including Nigeria, which launched its centralized digital currency in October 2021. We know that countries such as European Union countries, Canada, Brazil, and the United States are also considering launching digital centralized currencies in the near future.

In fact, the European Union is currently considering a legal framework for a digital euro. The Atlantic Council’s Central Bank Digital Currency Tracker is known to be conducting research on the subject in Canada, Brazil, the United States and other countries. 1

Undoubtedly, fintech technologies have a major impact on the creation and use of centralized digital currencies, the use of which is expected to become more widespread in the near future.

The opportunities that financial technology tools are expected to offer in terms of developing, using and securing centralized digital currencies are as follows:

- Providing infrastructure and security by providing digital wallets for storage transactions,

- Implementing advanced security measures such as multi-factor authentication,

- Implementation of data management tools for effective transaction tracking,

- Access to real-time market data sources,

- Developing data analytics tools specific to risk assessment,

- Ensuring compliance with legislation and transaction auditing.

At What Stage Are the Digital Turkish Lira Studies?

Drawing attention to the fact that the centralization feature constitutes a source of resentment in the eyes of the public and markets, the then CBRT Governor Hafize Gaye Erkan made the following statement in September 2023:

“The ultimate power of digital money comes not from being just digital money, but from being a monetary technology issued by a central bank.” 2

Following this statement, in the last days of 2023, the CBRT published the Digital Turkish Lira First Phase Evaluation Report and shared the details of the Central Bank Digital Currency and the Digital Turkish Lira with the public.

Considering digital money as an important part of the rapidly developing financial technologies ecosystem in Turkey, the CBRT aims for the Digital Turkish Lira to be an important building block in the growth of the financial technologies ecosystem in Turkey.

The Rise of Buy Now Pay Later (BNPL)

Buy Now Pay Later (BNPL) is a financing option that has gained great popularity around the world.

The BNPL model, which is a flexible financing method that allows interest-free payment of purchased products and services in the long term, is making a name for itself in our country as well as all over the world.

In fact, according to the latest research by Grand View Research, the BNPL market is expected to grow by 26.1% annually between 2023 and 2030. 3 According to the report prepared by Global Data, the BNPL market size is estimated to be $565.8 billion by 2026. 4

As can be seen, it is clear that this model, which started to be on the agenda around the world in the early 2000s and is currently being actively used in our country, will be on the radar of both consumers and businesses that accept online payments in 2024.

The countries that have adopted the BNPL model the most are Australia and Sweden. Other countries where BNPL has been adopted to a significant extent include China, Finland, Germany, the Netherlands, New Zealand, Norway, Singapore, the United Kingdom and the United States.

The consumer profile in countries where BNPL usage is widespread is mostly made up of Generations Y and Z. The model, which appeals to younger and more tech-savvy individuals, is generally the priority for those who do not have a credit card. 5

The BNPL model, which brings opportunities such as increased conversion rates, reduced cart abandonment rates and improved customer experience processes for brands, also provides significant payment convenience for end users.

Shopping Credit Usage Becomes More Common

It is anticipated that shopping credit solutions, which have been frequently used recently to provide consumers with payment in installments and ease of payment, will become even more widely used in the coming period.

The working principle of the shopping credit method is as follows: The application result of the online shopping credit, which can be used by anyone who does not have a credit card, does not want to use a credit card for shopping, or whose spending limit is insufficient for payment, is instantly sent to the customer. Thus, customers who choose the payment plan they want from the bank they want have the freedom to make payments with the credit limit offered to them.

The lack of credit card installment shopping opportunities or the decrease in installment amounts due to regulations in some sectors has accelerated the integration of shopping credit payment options on their platforms by brands operating in this field.

This situation is the reason why people who want to avoid filling their credit card limits and have easy payment options even for products that do not have the option of installments prefer brands that are integrated with shopping credit.

AI-Driven Personalized Financial Services

Advances in artificial intelligence and data analytics, which have been popular for a long time, are becoming a fintech trend that makes it easier to deliver a highly personalized experience in financial services. Thus, fintech products and fintech companies can offer customized budgeting, savings and investment advice.

Common usage areas of artificial intelligence in the fintech world are as follows:

- Personalized financial recommendations: Artificial intelligence-powered assistants, especially from fintechs operating in the investment vertical, analyze individual data and financial goals to provide customized recommendations for investing, saving, and financial management.

- Data-driven insights: AI can be used to optimize decision-making, streamline product purchasing processes, and adapt marketing strategies accordingly.

- Digital assistants: AI-powered chatbots and assistants help ease the burden on support teams by providing personalized financial advice 24/7. Additionally, Natural Language Processing (NLP) simplifies customer interaction by enabling chatbots to understand customer questions and provide accurate answers.

- Fraud prevention: AI is a major preventative in today’s increasingly complex cyber threat landscape by monitoring customer behavior, spending habits, and location to detect and prevent suspicious transactions.

Number of Users is Increasing in Mobile Payments

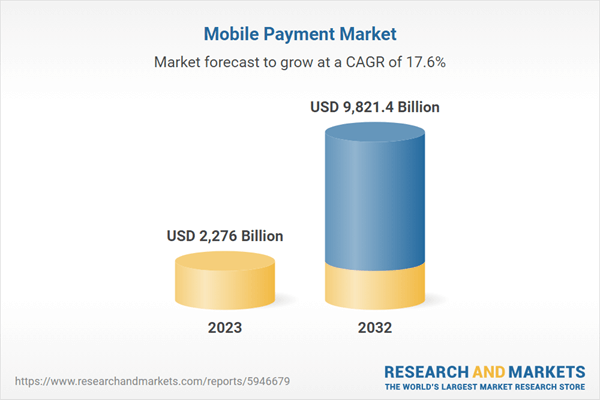

As smartphone usage increases, so does the use of mobile payments. According to Insider Intelligence’s November 2023 forecast, mobile purchases are expected to account for 44.6% of total U.S. retail e-commerce sales in 2024. 6

According to the same study, the share of mobile commerce in total retail will reach 8.7% by 2026. 7 This also highlights the popularity of mobile payments in 2024. According to Juniper Research, the number of contactless mobile payment users is expected to exceed one billion by the end of 2024. 8

With the rise of mobile commerce, the use of digital wallets is expected to become widespread by the end of 2024. Of course, this trend comes from the convenience offered by the mobile payment method.

Open Banking & API Integration Becomes Widespread

Open banking, a business model that enables the development of new products and services by sharing banking data with third-party banks and institutions via APIs (Application Programming Interfaces) and with the explicit consent of the customer, has been at the forefront of fintech trends for a long time.

According to a research report published by Spherical Insights & Consulting, the Global open banking market size is valued at USD 20.6 billion in 2022 and the worldwide open banking market is expected to reach USD 164.8 billion by 2032. 9

According to Fintech Times, the adoption of open collaboration between fintechs and banks allows users and companies to benefit from seamless data sharing, increasing the efficiency and speed of financial services.

Additionally, open banking improves customer experience by enabling the creation of personalized financial services by sharing data through standardized APIs.

As a result, the number of API integrations for open banking is expected to increase by 645% globally by the end of 2024. 10

We Will See Embedded Finance Applications More Frequently

Embedded finance, also known as embedded banking, is expected to grow rapidly in 2024. Within the scope of these applications, we see non-financial companies such as online shopping platforms and even social media giants integrating financial services directly into their existing platforms.

These applications, which enable users to manage their finances easily without leaving the familiar interface of widely used applications, eliminate the need to switch between multiple applications. They offer a smooth and user-friendly experience for the end user.

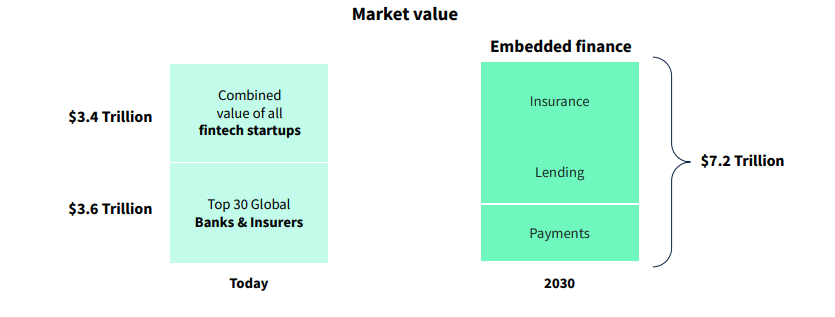

The study by Dealroom predicts that the embedded financing solutions market will reach a value of $7.2 trillion by 2030. 11

This growth in embedded finance is driven by a confluence of other fintech trends, including the rise of open banking, the increasing adoption of mobile wallets, and the growing demand for personalized financial services.

Decentralized Finance (DeFi) and the Use of Blockchain

DeFi, defined as decentralized finance that enables financial transaction management without third parties, enables services such as lending and investment by integrating cryptocurrency and blockchain technology without traditional intermediaries such as banks or other financial institutions. Through DeFis, both end users and businesses can benefit from many of the services supported by banks, such as using credit, lending, purchasing insurance, trading derivatives or swapping assets.

Basic Working Principle of DeFi

The DeFi system is based on blockchain technology and generally uses P2P (peer-to-peer) technology to create a decentralized financial network. Cryptocurrencies are used to perform the financial transactions we mentioned above. These currencies are managed and stored in many different wallets on the blockchain network. Wallets are supported by different block chains on the blockchain network.

The financial services performed are carried out using code snippets called smart contracts, which are stored and executed on the blockchain network. These codes allow transactions to be executed automatically. For example, sending money is executed by the smart contract code, and the money is sent only if the smart contract conditions are met.

DeFis are widely used around the world due to its advantages such as security and accessibility, personalized experience, low cost, and fast transaction capacity.

So much so that, according to the statement made by Grand View Research, the value of decentralized finance was determined as 13.61 billion USD in 2022. This figure is expected to rise to 231.19 billion dollars by 2030. 12

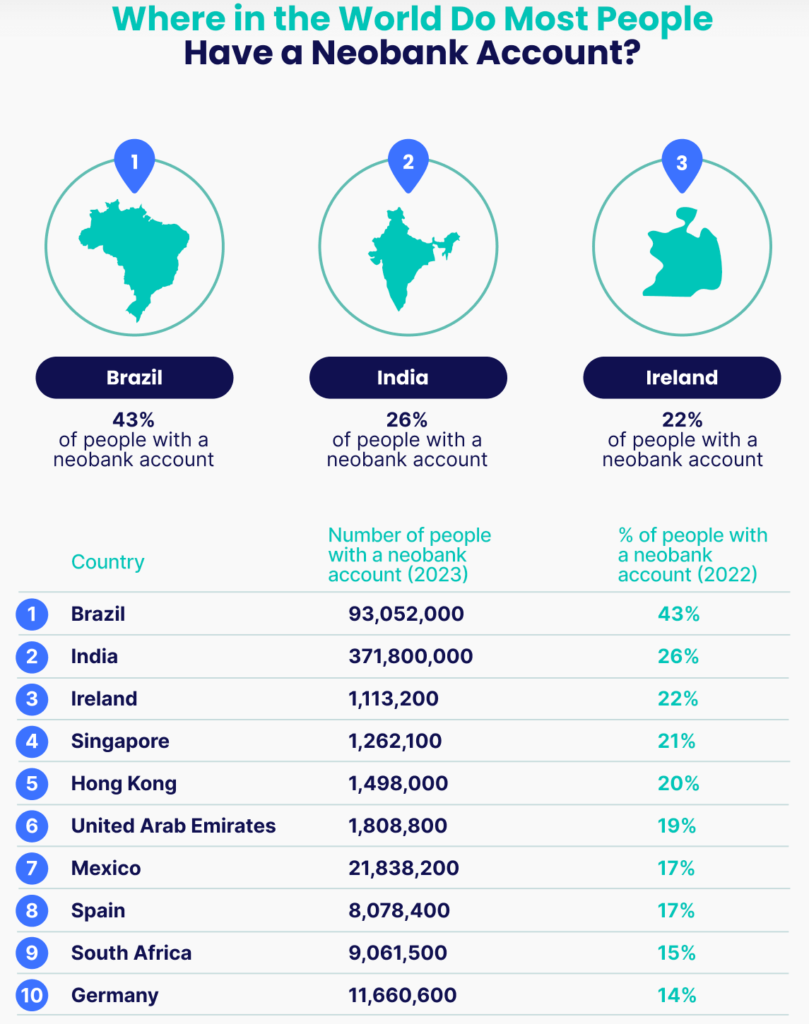

The Rise of Neobanks

Neobanks, the new generation banking system that enables all transactions related to financial institutions to take place in a digital environment, appear as financial technology companies without physical branches.

When we look at examples of neobanks around the world, we see that they are established in partnership with a traditional bank or financial institution, but the physical branches of the banks that are partnered with do not serve as branches of neobanks. Neobanks offer their products and services through digital channels. Although neobanks, which adopt a completely branchless banking model and do not have physical branches at any point, were initially difficult for users to adopt, in the age where many services are becoming digital, neobanking also convinced users in a short time.

In fact, almost every banking transaction can be done through these applications. Neobanks, which reduce the need for physical branches, can directly address the banking needs of users. Although it varies depending on the neobank in question, the transactions that can be done as a neobank user can be listed in general terms as follows:

- Payments for personal and corporate bills, credit cards, etc.

- Money transfers such as EFT, Wire Transfer and FAST

- Opening term and demand deposit accounts

- Creating a virtual card

- Opening foreign exchange and gold accounts

- Using an overdraft account

- Using consumer loans

- Payment, withdrawal and deposit via QR code

The neobank sector has seen rapid growth in recent years, matching the increasing demand for digital financial services.

The report prepared by Statista Market Insights in 2023 predicts that the total transaction value of neobanking will reach $2.60 trillion by 2027. It also predicts that there will be a penetration rate of 15.5% in 2023 and this rate will increase to 22.8% in the next five years. 13

Developments in Regtech Will Become Even More Important

Regulatory Technology (Regtech) in its most general form refers to the use of advanced technologies to simplify regulatory compliance procedures in any sector where regulatory requirements arise. Regulatory technologies in Turkish aim to facilitate compliance with technological applications that are added to our lives every day.

Especially due to the international usage areas offered by new generation technologies, the compliance of these technologies with the legislation of different countries is of critical importance. The operational and financial obligations of each country to comply with its own controls and regulations, especially in banking, finance, communications and energy, and the penalties imposed in case of non-compliance, accelerated the emergence of regtech companies.

Today, regtech provides companies with technological solutions to their obligations arising from legislation, helping them act in accordance with regulations and compliance requirements while conducting in-house compliance processes, audits and risk workflows.

For example, regtech applications ensure compliance with data privacy regulations in healthcare or monitor environmental laws in the energy sector. However, today, the financial services sector is the main consumer of regtech solutions.

According to Juniper Research, the adoption of regtech solutions in banks will result in cost savings of approximately US$460 million between 2020 and 2025.14

How is Regtech Used in Banking and Fintech?

Regtech solutions are typically used across a variety of banking and financial services functions, including regulatory compliance and reporting, risk management, online identity verification, transaction monitoring and auditing processes.

Regulatory Compliance: The main reason why regtech has become so popular is that it helps financial institutions simplify their regulatory processes.

Regulatory Reporting: Regtech solutions alert banks to real-time regulatory reporting changes so they can meet their reporting obligations and stay compliant with regulatory requirements. This allows financial institutions to automate the process of collecting and providing their data to meet compliance requirements, making this process less costly and time-consuming.

Risk Management: Regtech solutions can identify and manage risks before they occur. Regtech software can track high-risk incidents and predict potential fraudulent activity by analyzing scenarios based on past activity and behavior.

Online Identity Verification: Regtech solutions can help financial institutions more accurately and quickly determine customer identities and verify them using KYC procedures.

Suptech, which is the abbreviation for audit technology, refers to the technology that supports supervisory authorities in controlling and monitoring certain sectors.

Regtech and suptech, while similar and using similar technologies, differ in their focus. Regtech focuses on helping financial institutions comply with regulatory requirements, while suptech aims to assist regulators in overseeing and monitoring financial institutions.

According to research by Market & Market, the regtech market is estimated to grow from $7.6 billion in 2021 to $19.5 billion by 2026. 15

As can be seen, regtech, a fintech trend that brings many advantages for both technology players and users due to regulatory needs, will find even more areas of use in the coming period.

The Rise of Banking Technologies as a Service

Among the fintech trends, Banking as a Service (BaaS) emerges as a model that enables third-party companies to provide financial services by leveraging the infrastructure and capabilities of Electronic Money Institutions (EMI) to reduce complex and lengthy processes. It enables non-banking institutions to access and use technologies through APIs and other software integrations.

Offering a fast and accessible path to financial services, BaaS technologies allow businesses seeking financial services to manage multiple services through a single integration that offers a simplified back-end process. Businesses are using BaaS to optimize their operations and reduce manual processes and expenses, while increasing payment options to better engage with their customers.

In addition to businesses, end users also benefit significantly from banking as a service solutions. Users benefit from continuously improving services and experiences, from financial inclusion to personalized shopping experiences.

According to research by the World Bank, there were 1.4 billion people worldwide who had no contact with a bank in 2023. The widespread use of BaaS products is thought to facilitate users’ access to different banking products and services through alternative platforms and applications. 16

According to another study, the BaaS market was worth $15.9 billion in 2023. This figure is expected to record a compound annual growth rate (CAGR) of over 17% by 2032. 17

Payment Orchestration Platforms Will Become Game Makers in 2024!

The significant popularity of e-commerce all over the world and the increasing competition in the market have made it necessary for brands to make some optimizations in the payment step. Knowing how important the payment step is for the customer experience, retailers prioritize providing their customers with a simple, fast and secure payment experience.

In addition, the diversification of options in the payment world, customers’ turning to wider options at the payment stage and brands’ desire to embrace diversity in payment processes are causing orchestration solutions to become widespread around the world.

Payment Orchestration Market Volume Expands

Payment orchestration platforms, also referred to as Payment Orchestration Platform (POP) or Payment Orchestration Layer (POL), are expected to become a game changer in the payment world in the near future.

According to research by ReportLiker, the payment orchestration platform market volume is expected to reach $3.7 billion by 2028, growing at a CAGR of 22.4% during the forecast period. 18 Another study predicts that the global payment orchestration market will grow at a CAGR of 24.7% between 2023 and 2030. 19

The payment orchestration platform market size is regionally based on North America, Europe, Asia Pacific, and LAMEA.

Businesses Aware of the Benefits of Payment Orchestration Platforms

According to a survey conducted by Edgar, Dunn & Company of senior executives of businesses that accept online payments, 84% of respondents work with more than 20 payment service providers, and 75% of executives say they want to be able to manage these service providers from a single source.

According to the study, the awareness of these managers about the advantages offered by payment orchestration platforms is 74%.

Payment Orchestration Platforms Open the Door to Payment Options for Businesses!

According to an analysis by Stripe , 85% of e-commerce customers abandon online shopping when their preferred payment method is not an option.

Today, users find payment options that only allow them to pay by card insufficient. Alternative payment methods, including options such as BNPL and shopping credit, are among the payment preferences of customers at this point. This also prioritizes businesses to increase the payment options they offer to their customers.

Payment orchestration platforms allow businesses to work with any payment service provider and alternative payment methods from a single point with the ready-made integrations they contain. Businesses that want to increase the options they offer during the payment step do not have to deal with the burden of separate integrations for each payment method with the ready-made integration opportunity offered by payment orchestration platforms.

In this way, businesses can expand their customer base and achieve a more reliable brand profile.

Payment Orchestration Platforms Reduce Cart Abandonment Rates for Businesses

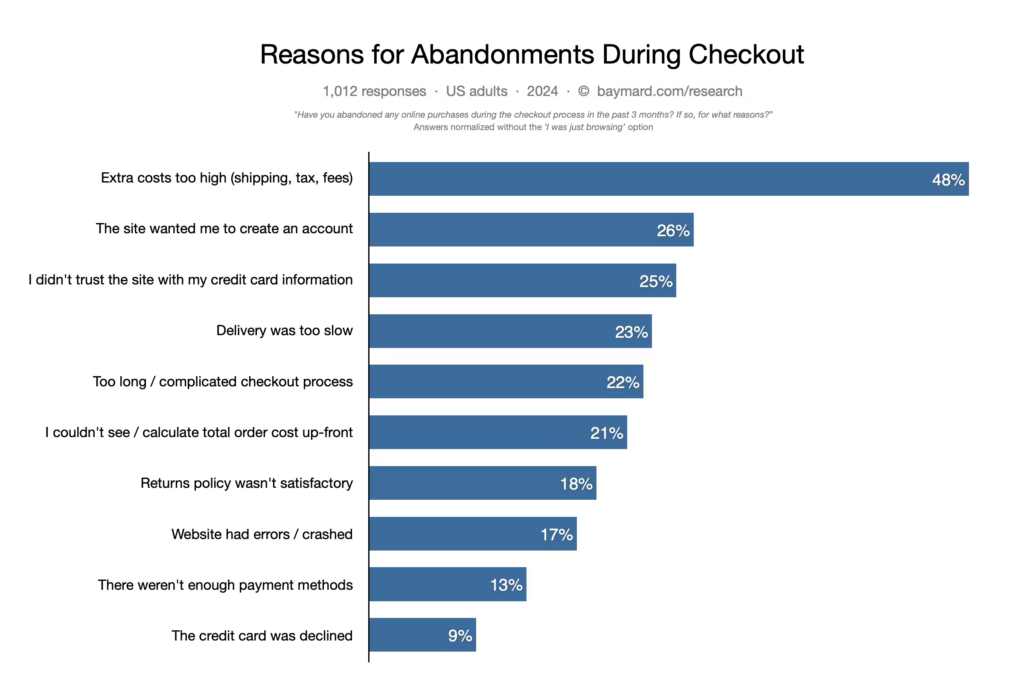

The Baymard Institute’s research on shopping cart abandonment rates reveals the impact of interruptions and lack of validation at checkout on cart abandonment rates.

Accordingly, the rate of cart abandonment due to payment pages that are too long and do not provide a smooth experience was determined as 18%. 21

Payment orchestration platforms not only allow businesses to work with any payment service provider from a single point, but also stand out with their solutions that increase conversion rates and reduce cart abandonment rates.

At this point, payment orchestration platforms make the payment step smooth for customers with the fluid payment experience they offer. They eliminate cart abandonment behaviors that may occur due to system payment errors or interruptions in virtual POS during the payment step.

Businesses Reduce Costs with Payment Orchestration

Another advantage that payment orchestration platforms offer to businesses is reducing costs arising from payment processes.

At this point, with the smart and dynamic routing mechanisms offered by orchestration solutions, businesses can direct payment requests coming to their platforms in the most advantageous way for themselves.

{kind=link}